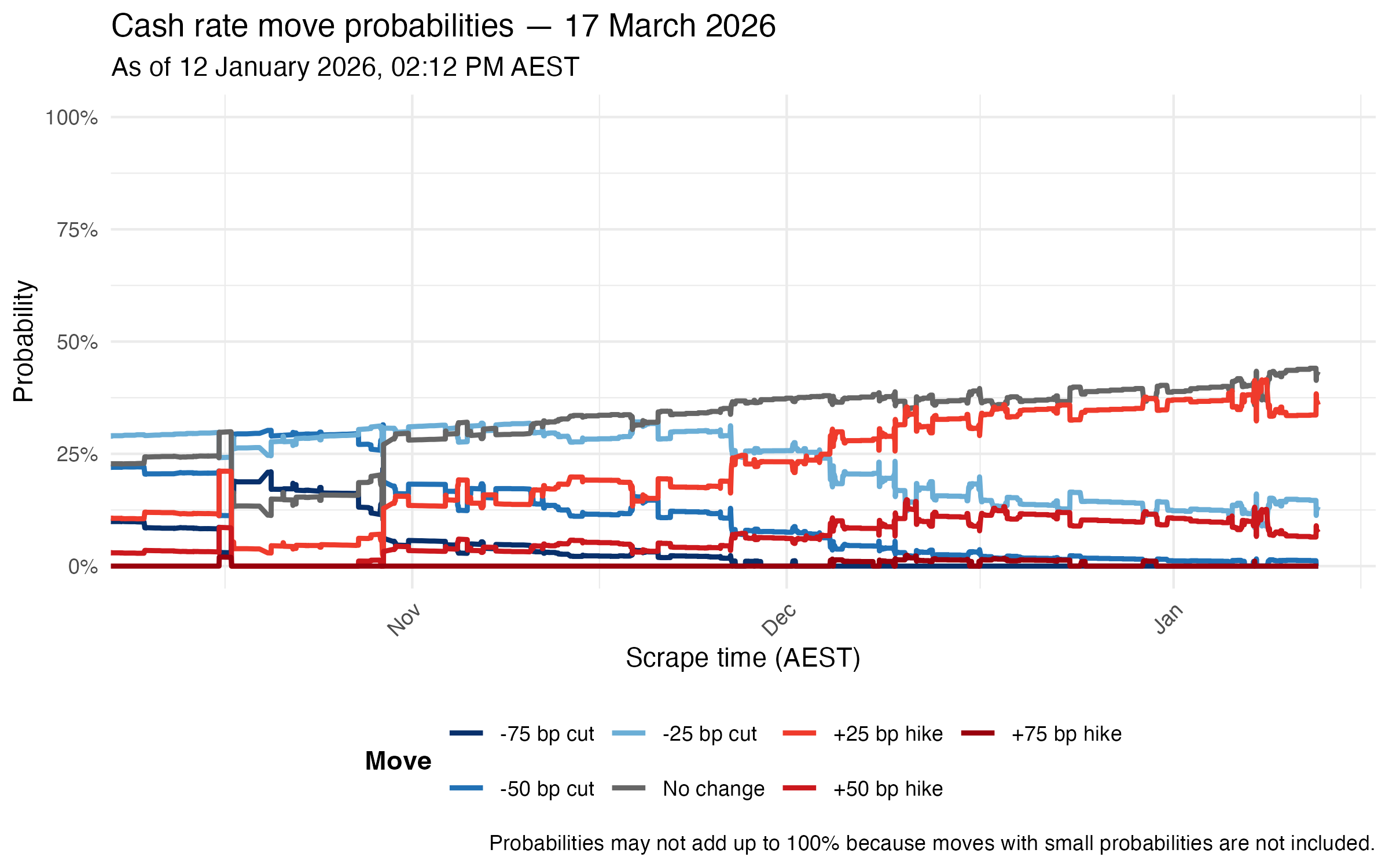

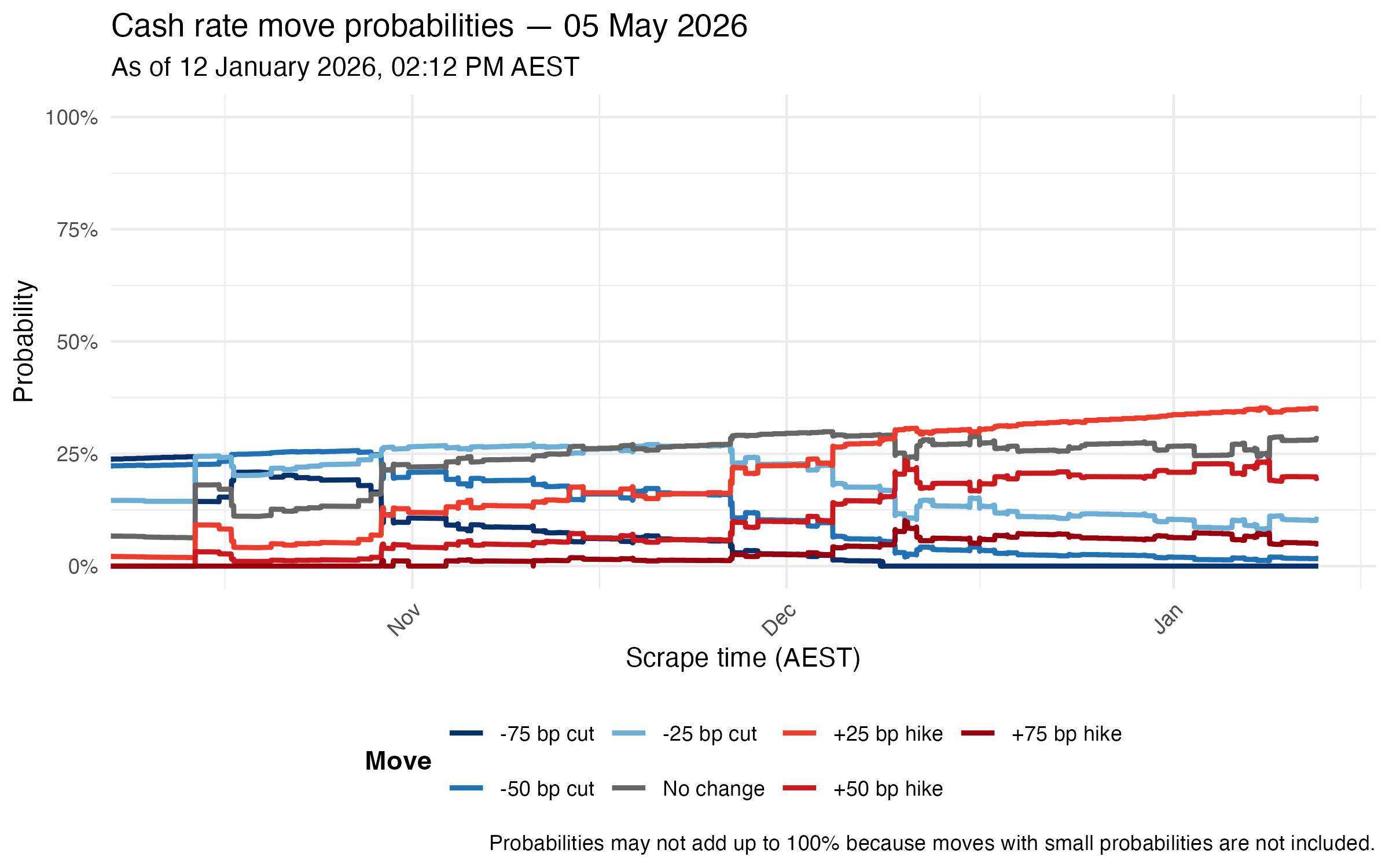

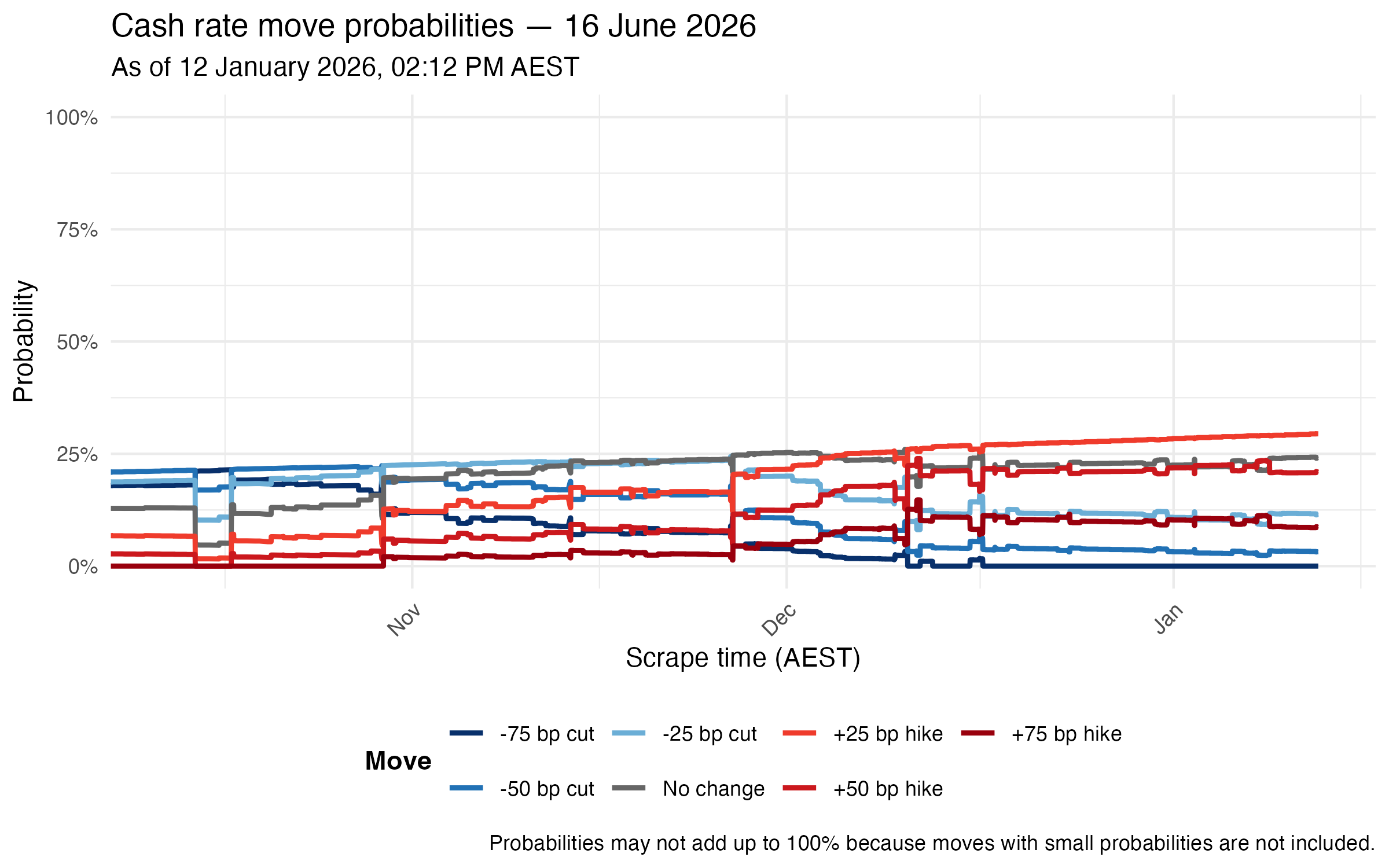

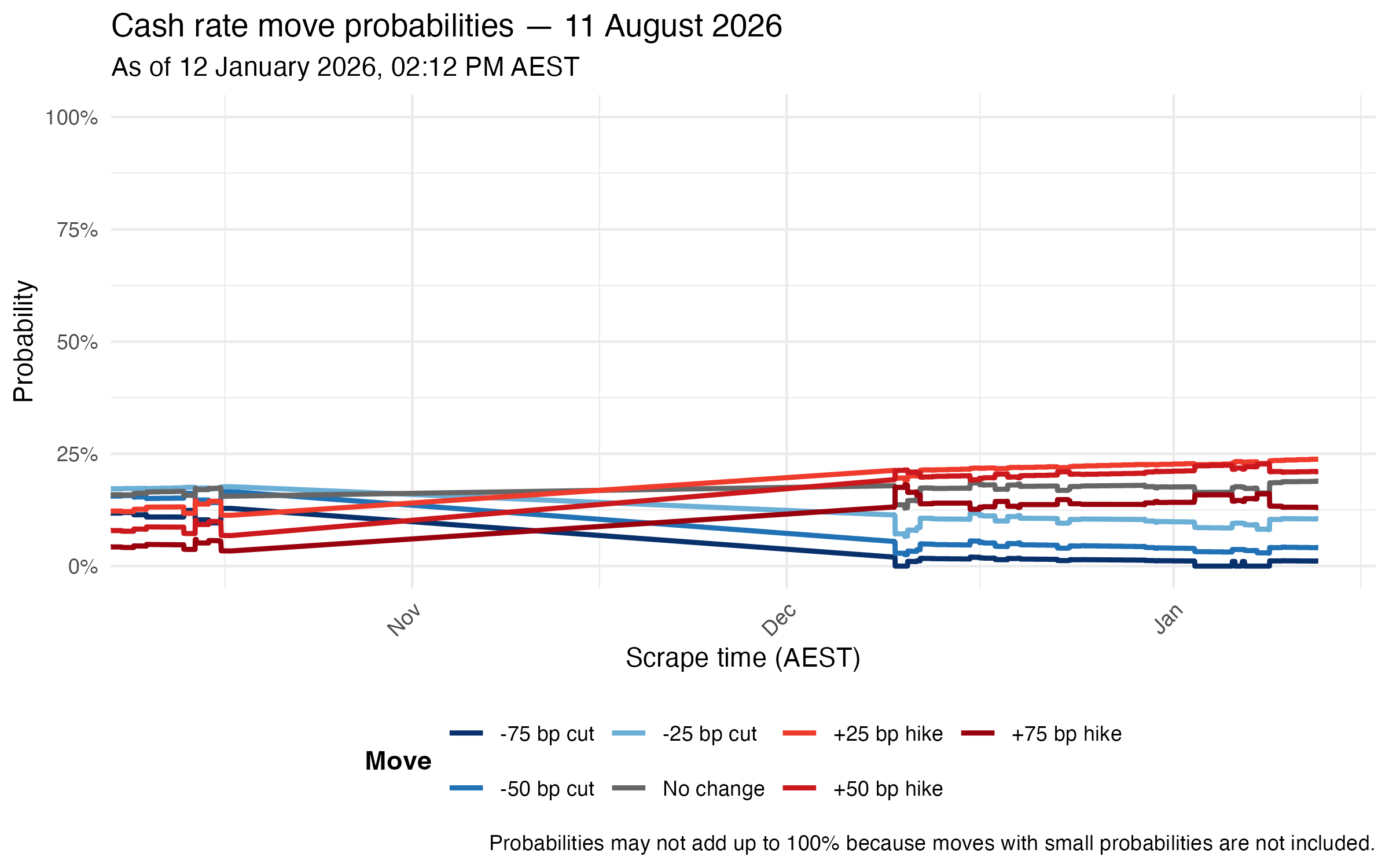

Cash Rate Target Probabilities By RBA Meeting

05 May 2026

16 June 2026

11 August 2026

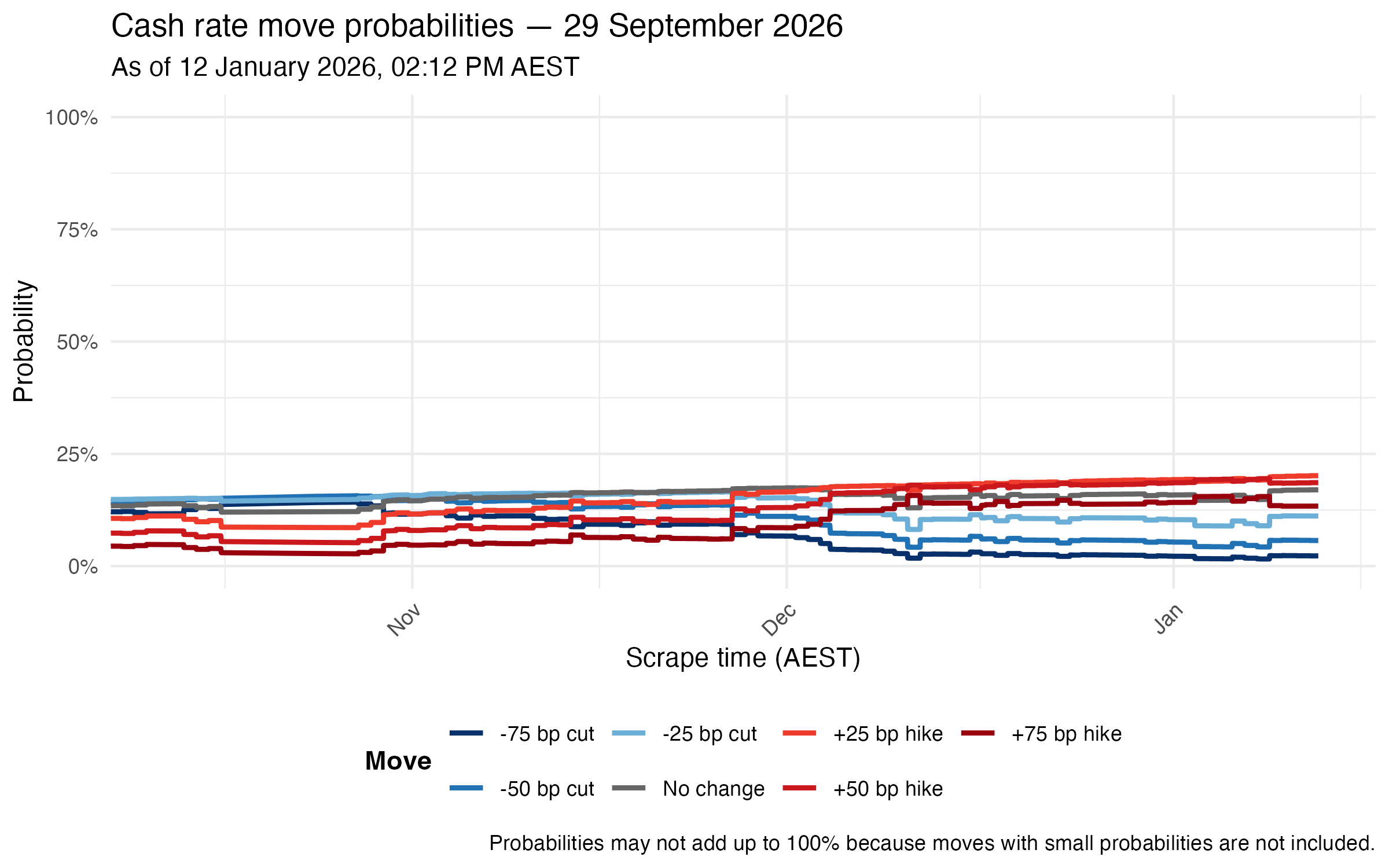

29 September 2026

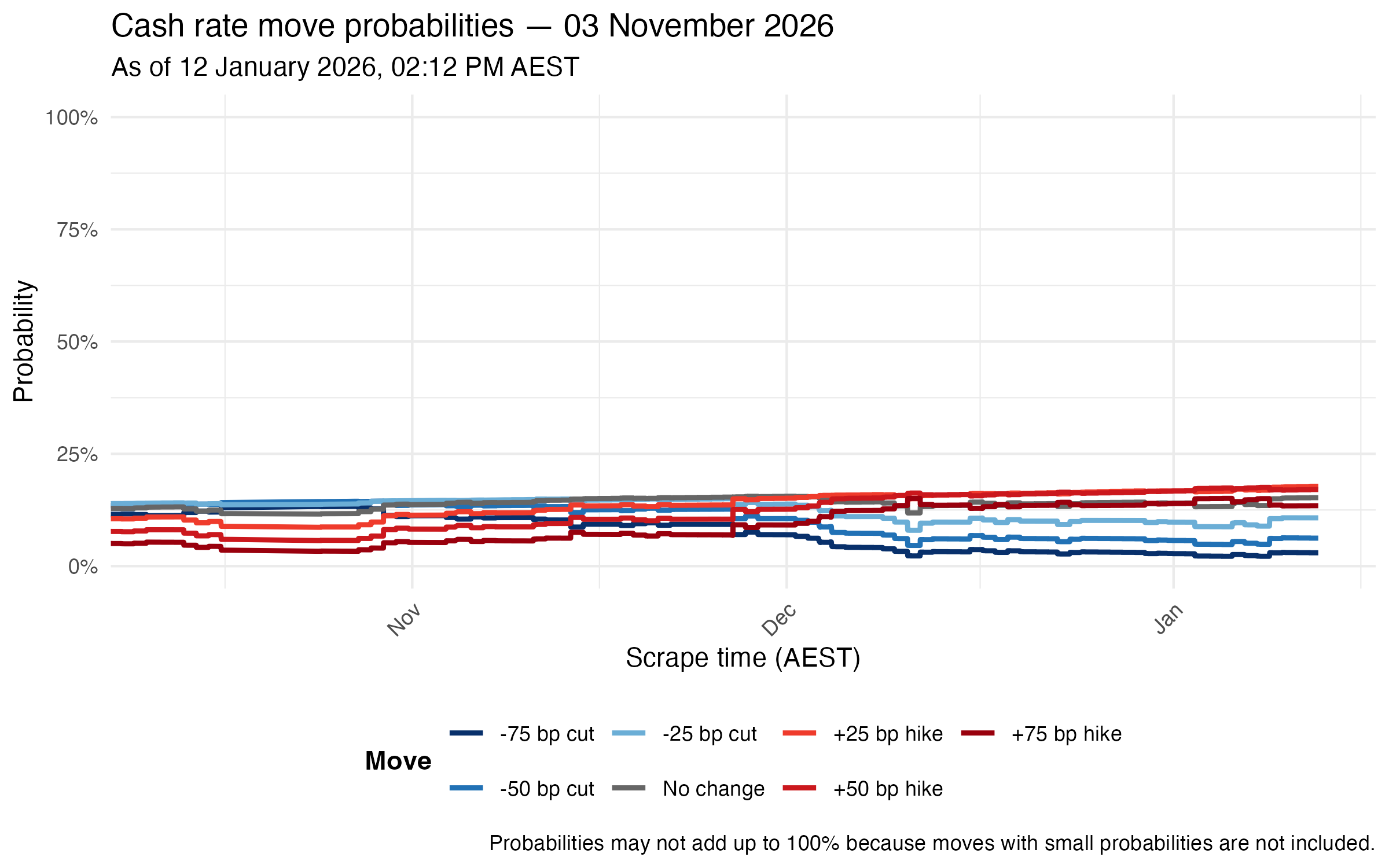

03 November 2026

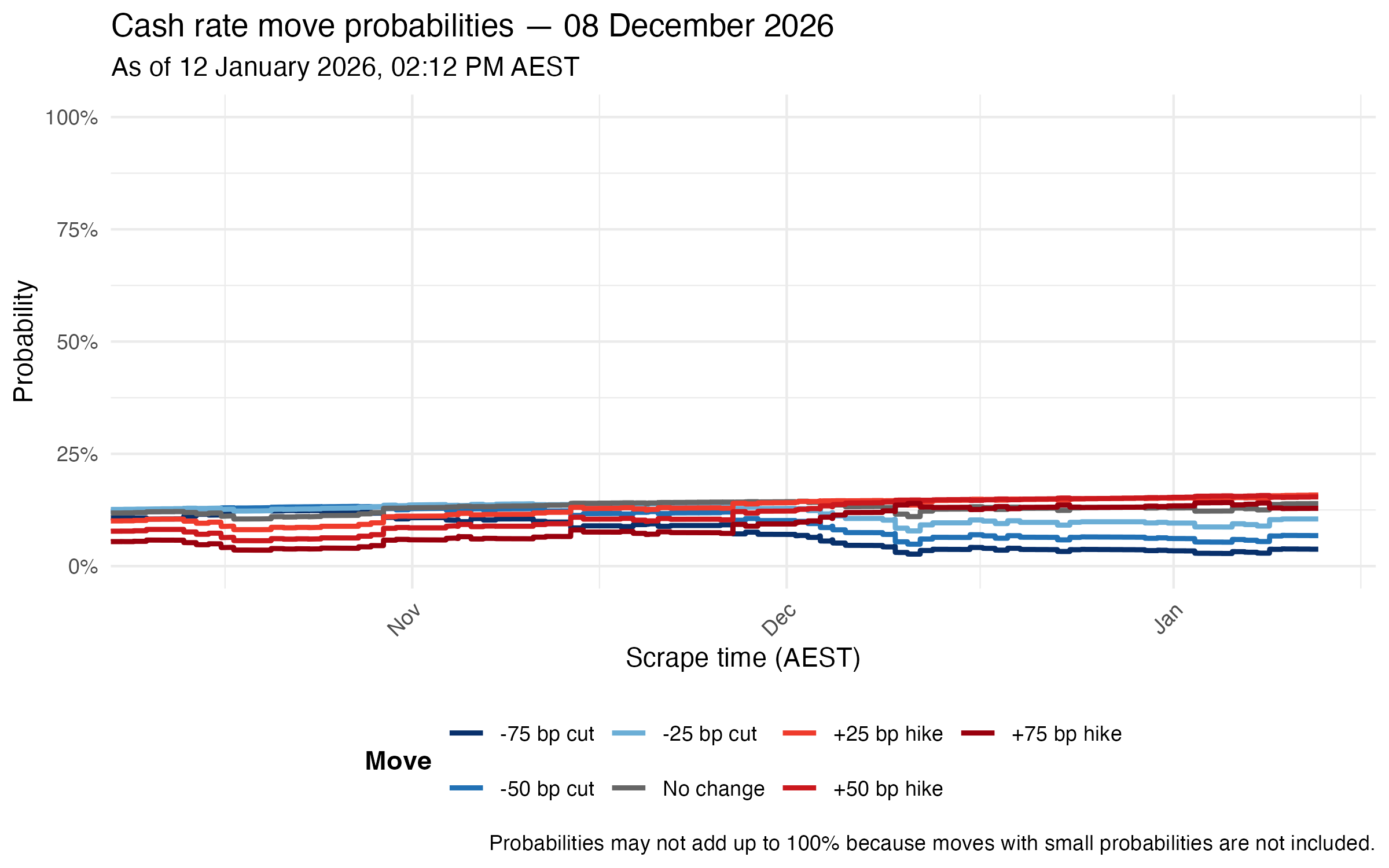

08 December 2026

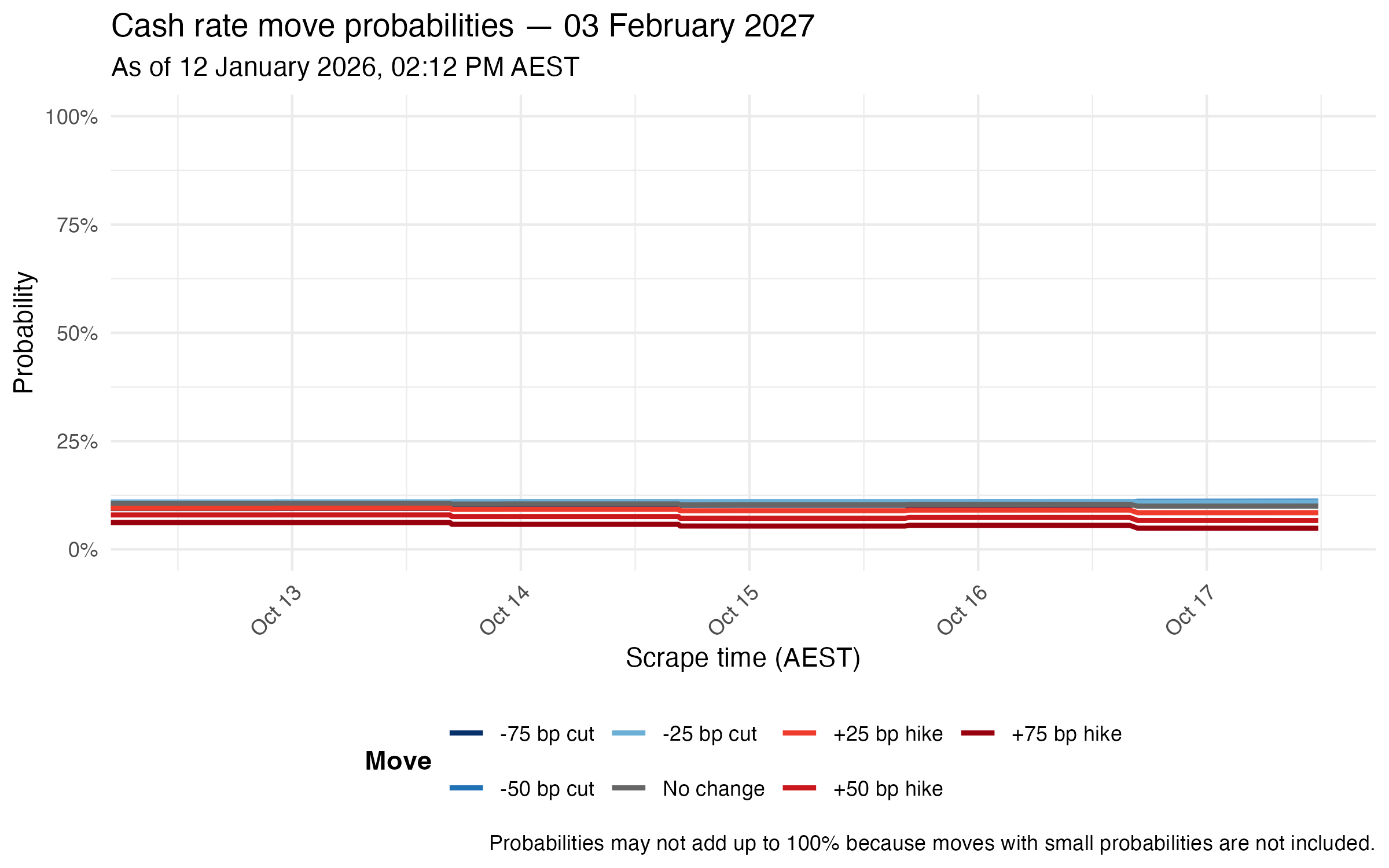

03 February 2027

17 March 2027

This website is built by Zac Gross and provides a daily snapshot of futures-implied expectations for the Reserve Bank of Australia's cash rate, based on ASX 30-day interbank futures data and historical data. These expectations update automatically based off code by Matt Cowgill.

This chart shows the market-implied probability of different cash rate outcomes at the next RBA meeting, hover over the chart to explore daily probabilities. View static version →

Interactive forecast paths around RBA meetings, CPI releases, and labour force publications. Hover to inspect each scrape and use the scroll wheel or pinch gesture to zoom the timeline. Open full-screen → View static version →